Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Balancing Medicare and Work-Based Insurance

The number of working Americans age 65 and older dropped by 1.1 million during the first three months of the pandemic and has been slower to recover than other age groups. Even so, more than 10.8 million workers are eligible for Medicare, and the number is likely to grow as 10,000 baby boomers turn 65 every day until 2030.1–2

Some employers — especially small businesses — may require employees or covered spouses to enroll in Medicare when they are eligible in order to retain their employer-sponsored health insurance. But many workers who are eligible for both types of coverage can choose one or the other, or both. To make an informed decision, it’s important to understand an array of rules and other considerations regarding costs and coverage.

Primary Insurance vs. Secondary Insurance

If an employer has 20 or more employees, the employer health coverage is primary and would pay first for covered expenses. Medicare is secondary and may pay for some expenses not covered by the employer coverage. Employers with 20 or more employees must offer the same health insurance benefits to employees age 65 and older that are offered to younger workers. The same is true of spousal benefits, if offered.

If an employer has fewer than 20 employees (and is not part of a multi-employer group for health insurance), Medicare would be primary and the employer coverage would be secondary, which is why small businesses may require eligible employees or spouses to enroll in Medicare in order to have employer-sponsored coverage.

Ask your employer if you have questions about your coverage at age 65.

Part A Hospital Insurance and HSAs

Medicare Part A helps pay for inpatient hospital care as well as some skilled nursing facility, hospice, and home health care. Because it is free for most people, consider enrolling in Part A even if you have employer coverage. It could be helpful to have both types of insurance to fill any coverage gaps. However, if you have to pay for Part A, you may want to wait before enrolling.

If you have a high-deductible health plan through work, keep in mind that you cannot contribute to a health savings account (HSA) after you enroll in Medicare. The HSA is yours, even if you can no longer contribute to it, and you can use the tax-advantaged funds to pay Medicare premiums, along with other qualified medical expenses. So it might be helpful to build your HSA balance before enrolling in Medicare.

Whether you should opt out of premium-free Part A in order to contribute to an HSA depends on what you consider to be more valuable: secondary hospital insurance coverage or tax-advantaged contributions. HSA funds can be withdrawn free of federal income tax and penalties provided the money is spent on qualified health-care expenses. HSA contributions and earnings may or may not be subject to state taxes.

If you claim Social Security benefits, regardless of your work status, you will be enrolled automatically in Part A and will not be able to contribute to an HSA.

Part B and Part D

Medicare Part B medical insurance, which helps pay for physician and outpatient expenses, requires premium payments, so it would be wise to compare the costs and benefits of Medicare to your employer’s plan. If you’re satisfied with your employer coverage, you can generally wait to enroll in Part B. The same is true of Medicare Part D, which helps pay for prescription drug costs.

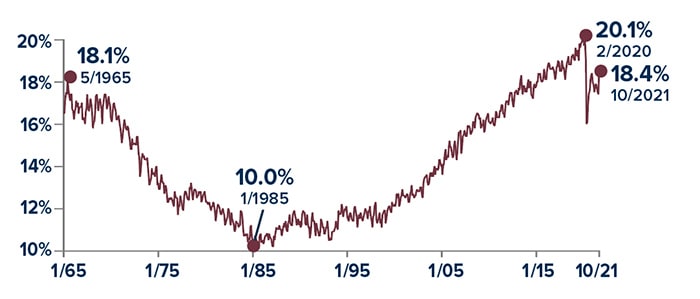

Working After 65

After Medicare became law in July 1965, the share of Americans aged 65 and older who continued working steadily declined. Beginning in 1985, that trend reversed as fewer workers relied on traditional pensions, more people shifted into knowledge-based jobs, and lifespans increased. During the early months of the pandemic, employment among this age group fell sharply, and it remains unclear whether participation will return to its pre-pandemic peak.

If you want it more formal, more conversational, or more SEO-optimized, say the word and I’ll tweak it.

Medicare Enrollment Periods and Penalties Explained

Understanding Medicare enrollment periods and penalties helps you avoid higher healthcare costs later. Medicare enforces strict enrollment timelines. Missing a deadline can increase your premiums for life. When you know the rules early, you can enroll with confidence and protect your budget.

Medicare Enrollment Periods and Penalties Overview

You can enroll in premium-free Medicare Part A anytime after eligibility without a penalty. However, Medicare enrollment periods and penalties apply if Part A requires a premium or if you delay Medicare Part B enrollment.

Late enrollment penalties may apply if you delay enrollment in the following plans:

Premium-based Medicare Part A

Medicare Part B

A Medicare Advantage Plan instead of Original Medicare

Each delay can increase your long-term healthcare costs.

Medicare Enrollment Periods and Employer Coverage

Medicare enrollment periods and penalties do not apply when you have health insurance through current employment. This protection remains valid if you enroll in Medicare within eight months after your job ends.

Key Rules for Employer Coverage

Coverage must come from active employment

The eight-month window begins after your last working day

The insurance end date does not change this timeline

If you miss this special enrollment period, Medicare may apply permanent penalties.

Medicare Enrollment Periods and Penalties for Part D

You can enroll in a Medicare Part D prescription drug plan during the two full months after employer coverage ends. That employer plan must qualify as creditable prescription drug coverage.

Most employer-sponsored plans meet this requirement.

What Happens If You Miss the Part D Window

You must wait for the annual open enrollment period

Open enrollment runs from October 15 to December 7 each year

Medicare may add a late penalty to your Part D premium

These costs often last for the rest of your life. This fact shows why Medicare enrollment periods and penalties deserve close attention.

Why Medicare Enrollment Periods and Penalties Matter

Medicare rules can feel confusing at first. Even a short delay can raise your premiums permanently. Understanding Medicare enrollment periods and penalties helps you avoid mistakes and make informed decisions.

For official and detailed guidance, review your options carefully at medicare.gov.

1) U.S. Bureau of Labor Statistics, 2021

2) U.S. Census Bureau, 2019

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.