Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Credit Scores Reach Record High

The average FICO® credit score in the United States reached a record high of 711 in 2020, even as the pandemic created widespread financial challenges. In fact, contrary to expectations, consumers improved their debt management after January 2020. As a result, total debt declined, credit usage fell, and late payments dropped.

This trend may reflect more cautious consumer spending in response to a struggling economy, as well as additional support from government stimulus programs. Even so, credit scores have continued to rise steadily over the past decade.

An Important Number

Your credit score plays a key role in loan approvals and borrowing terms for many financial transactions. For example, lenders use it not only for major purchases such as a home or car, but also for credit cards, insurance premiums, and home rentals. In some cases, employers may even consider credit history during the hiring process.

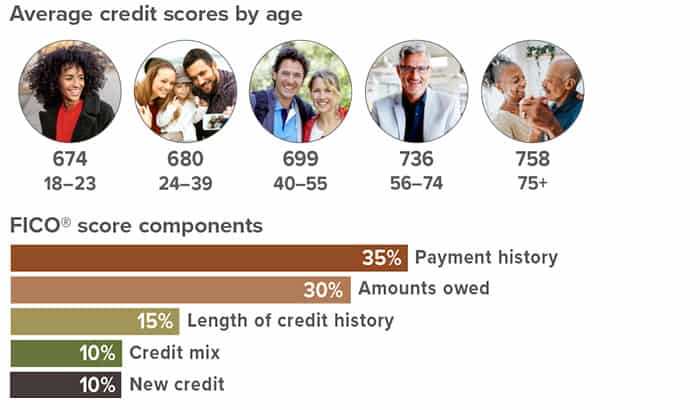

Most commonly, lenders rely on credit scores generated using algorithms developed by Fair Isaac Corporation (FICO). These three-digit scores range from 300 to 850. Additionally, all three national credit bureaus—Equifax, Experian, and TransUnion—calculate scores based on the information each agency maintains. As a result, your FICO scores may differ across bureaus, and you may also encounter non-FICO scoring models. Nevertheless, any version of your credit score generally provides a reliable picture of how lenders view your creditworthiness. Moreover, many major credit card issuers offer free access to credit scores and related information for account holders.

Tips to Improve or Maintain Your Credit Score

- To begin with, use at least one major credit card regularly and pay your accounts on time. In addition, setting up automatic payments can help prevent missed due dates.

- If you miss a payment, contact the lender promptly and bring the account current as soon as possible.

- At the same time, keep balances low on credit cards and other revolving debt, and avoid maxing out available credit.

- Furthermore, avoid opening or closing multiple accounts within a short period. Instead, use older credit cards occasionally to keep them active, and open new accounts only when necessary.

- Finally, monitor your credit report regularly to spot errors or potential issues early.

Older and Financially Wiser?

By law, you can order a free credit report annually from each of the three national credit bureaus at annualcreditreport.com or by calling (877) 322-8228. During the pandemic, all three bureaus are offering free weekly reports (extended through April 20, 2022). If you find incorrect information, contact the reporting agency in writing, provide copies of any corroborating documents, and ask for an investigation. For more information, visit consumer.ftc.gov/articles/0155-free-credit-reports.

1–2) Experian, December 8, 2020

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.