Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Don’t Let Debt Derail Your Retirement

Debt poses a growing threat to the financial security of many Americans — and not just college graduates with exorbitant student loans. Recent studies by the Center for Retirement Research at Boston College (CRR) and the Employee Benefit Research Institute (EBRI) reveal an alarming trend: The percentage of older Americans with debt is at its highest level in almost 30 years, and the amount and types of debt are on the rise.

Debt Profile of Older Americans

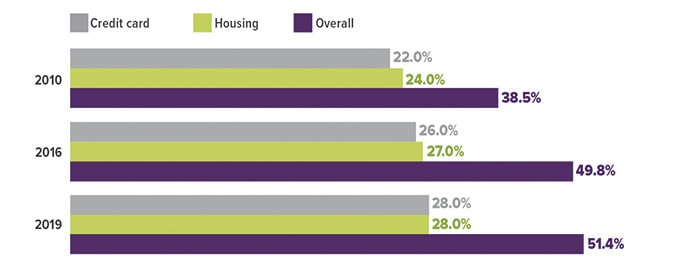

From 1998 to 2019, debt steadily increased among families with household heads age 55 and older. More recently, families led by adults age 75 and older have driven most of that growth. Between 2010 and 2019, the share of this older group carrying debt rose from 38.5% to 51.4. That figure marks the highest level since 1992. Meanwhile, debt levels among younger age groups either rose slightly or remained stable.

Mortgages make up the largest share of debt held by older Americans. In fact, housing debt represents about 80% of their total debt burden. According to EBRI, the median housing debt for adults age 75 and older climbed from $61,000 in 2010 to $82,000 in 2019. The CRR study also found that baby boomers carry heavier debt loads than earlier generations. In many cases, higher home prices and smaller down payments drove this increase. As a result, changes in interest rates, home values, and mortgage-related tax rules can strongly affect the financial stability of current and future retirees.

Credit-card balances represent the largest source of nonhousing debt among older Americans. In 2019, 28% of adults age 75 and older reported carrying credit-card debt, the highest level on record. During the same period, the median balance rose from $2,100 in 2010 to $2,700.

Medical debt also places pressure on older households. Often, unexpected emergencies create these balances. In the CRR study, 21% of baby boomers reported medical debt, with a median balance of $1,200. Among those managing chronic illnesses, one in six said prescription drug costs caused their debt.

Finally, student loans have become the fastest-growing debt category for older adults. Surprisingly, most older borrowers take on this debt to help children or grandchildren pay for college, not to fund their own education.

How Debt Might Affect Retirement

Studies from the CRR and EBRI warn that rising debt levels may not be sustainable for current and future retirees. In many cases, carrying high debt creates ongoing stress that harms physical health. Over time, these health issues can increase medical expenses and create even greater financial pressure. As a result, some individuals may enter a damaging cycle of debt and declining well-being.

Additionally, debt can delay retirement. Many workers postpone leaving the workforce simply to keep up with monthly payments. At the same time, retirees and near-retirees may feel forced to withdraw money from retirement savings earlier than planned. Unfortunately, doing so can weaken long-term financial security and reduce income later in life.

If you are already retired or close to retirement, consider reviewing your debt-to-income and debt-to-assets ratios. From there, aim to reduce those ratios gradually to improve financial stability. On the other hand, if retirement remains several years away, you may want to prioritize debt reduction alongside saving for retirement. By doing both, you can strengthen your overall retirement readiness.

Sources: Center for Retirement Research at Boston College, 2020; Employee Benefit Research Institute, 2020

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.