Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

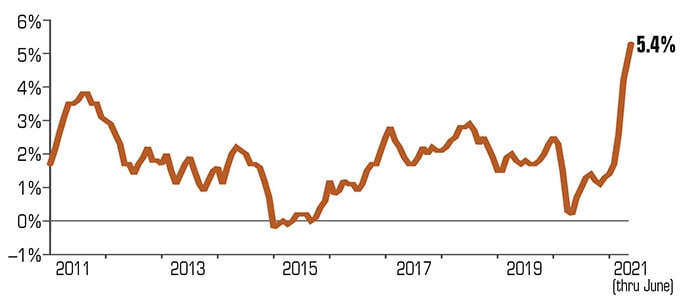

Following the Inflation Debate

During the 12 months ending in June 2021, consumer prices shot up 5.4%, the highest inflation rate since 2008.1 The annual increase in the Consumer Price Index for All Urban Consumers (CPI-U) — often called headline inflation — was due in part to the “base effect.” This statistical term means the 12-month comparison was based on an unusual low point for prices in the second quarter of 2020, when consumer demand and inflation dropped after the onset of the pandemic.

Inflation Pressures Emerge in 2021

However, clear inflationary pressures emerged in the first half of 2021. As vaccination rates increased, pent-up consumer demand surged for goods and services. Furthermore, stimulus payments and strong household savings fueled spending among consumers who previously had limited opportunities to spend. Many businesses that had shut down or reduced operations during economic closures could not scale up quickly enough to meet rising demand. Consequently, supply-chain bottlenecks combined with higher costs for raw materials, fuel, and labor led to noticeable price spikes.

Monitoring Inflation Trends

The Consumer Price Index for All Urban Consumers (CPI-U) measures the cost of a fixed market basket of goods and services. Therefore, it provides a useful snapshot of prices consumers pay when they purchase the same items over time. However, CPI-U does not account for changes in consumer behavior and can be heavily influenced by sharp price increases in specific categories.

For example, in June 2021, used-car prices rose 10.5% from the previous month and surged 45.2% year over year. As a result, this category alone accounted for more than one-third of the overall CPI increase. Meanwhile, core CPI, which excludes volatile food and energy prices, increased 4.5% year over year.

Preferred Inflation Measures Used by the Federal Reserve

When setting economic policy, the Federal Reserve relies more heavily on the Personal Consumption Expenditures (PCE) Price Index. Moreover, this measure is broader than the CPI and adjusts for shifts in consumer behavior, such as when consumers substitute less expensive items for costlier alternatives.

More specifically, the Federal Reserve focuses on core PCE, which removes food and energy prices. Through the 12 months ending in June 2021, core PCE rose 3.5%. Consequently, policymakers use this measure to gain a clearer understanding of underlying inflation trends.

Competing Viewpoints on Inflation

Many economic policymakers, including Federal Reserve Chair Jerome Powell and Treasury Secretary Janet Yellen, viewed the spring increase in inflation as largely driven by base effects and temporary supply-and-demand imbalances. Therefore, they expected inflationary pressures to be mostly transitory.

Nevertheless, some prices do not return to previous levels once they rise. Consequently, even short-lived inflation spikes can strain household budgets and reduce purchasing power.

In contrast, other economists argue that inflation could persist longer and produce more serious consequences. This group believes that loose monetary policy and trillions of dollars in government stimulus injected excessive liquidity into the economy. As a result, a strong economic expansion combined with sustained inflation could create a self-reinforcing cycle. In this scenario, businesses may raise prices in anticipation of higher future costs, while workers respond by demanding higher wages.

Consumer Price Index Overview

The Consumer Price Index (CPI-U) tracks monthly percentage changes compared with the previous year. Consequently, it remains a widely watched indicator for understanding inflation trends affecting consumers.

Until recently, inflation had consistently lagged the Fed’s 2% target, which it considers a healthy rate for a growing economy, for more than a decade. In August 2020, the Federal Open Market Committee (FOMC) announced that it would allow inflation to rise moderately above 2% for some time in order to create a 2% average rate over the longer term. This signaled that economists anticipated short-term price swings and assured investors that Fed officials would not overreact by raising interest rates before the economy has fully healed.7

In mid-June 2021, the FOMC projected core PCE inflation to be 3.0% in 2021 and 2.1% in 2022. The benchmark federal funds range was expected to remain at 0.0% to 0.25% until 2023.8 However, Fed officials have also said they are watching the data closely and could raise interest rates sooner, if needed, to cool the economy and curb inflation.

Projections are based on current conditions, are subject to change, and may not come to pass.

1, 3) U.S. Bureau of Labor Statistics, 2021

2) The Wall Street Journal, April 13, 2021

4) U.S. Bureau of Economic Analysis, 2021

5–6) Bloomberg.com, May 2, 2021

7–8) Federal Reserve, 2020–2021

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.