Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Is a High-Deductible Health Plan Right for You?

In 2020, 31% of U.S. workers with employer-sponsored health insurance had a high-deductible health plan (HDHP), up from 24% in 2015.1 These plans are also available outside the workplace through private insurers and the Health Insurance Marketplace.

Comparing an HDHP to a PPO

Although participation in high-deductible health plans (HDHPs) has increased rapidly, the most common option, covering nearly half of U.S. workers, remains the traditional preferred provider organization (PPO). Therefore, if you are considering enrolling in an HDHP or are already enrolled in one, it is important to understand several key factors when comparing an HDHP to a PPO.

Up-Front Savings

The average annual employee premium for HDHP family coverage in 2020 was $4,852, compared with $6,017 for a PPO. Consequently, this represents an annual savings of $1,165. Furthermore, many employers contribute to a health savings account (HSA), and both employer and employee contributions receive favorable tax treatment. Taken together, these features can result in meaningful savings that may be used to cover both current and future medical expenses.

Pay As You Go

In exchange for lower premiums, an HDHP requires you to pay more out of pocket for medical services until you reach the plan’s annual deductible. Therefore, understanding how costs are structured is essential.

Deductibles

An HDHP generally has a higher deductible than a PPO. However, PPO deductibles have been rising in recent years. As a result, it is important to compare the difference between deductibles and determine whether they apply per person or per family. Additionally, PPOs may have a separate deductible, or no deductible, for prescription drugs, whereas the HDHP deductible typically applies to all covered medical expenses.

Copays

PPO plans often include copays, allowing you to access certain medical services or prescription drugs for a fixed payment before meeting the deductible. In contrast, HDHP participants pay out of pocket until the deductible is met, though negotiated insurer rates may reduce costs. Therefore, comparing a typical copay with the negotiated rate for services such as doctor visits can help clarify potential expenses. Preventive care and certain preventive medications are often covered at no cost under both plans.

Out-of-Pocket Maximums

Most health insurance plans include annual and lifetime out-of-pocket maximums, after which the insurer covers all eligible expenses. HDHP maximums are often similar to those of PPO plans, though some PPOs have separate prescription drug limits. Consequently, if your medical costs exceed the annual maximum, your total out-of-pocket spending for the year may actually be lower under an HDHP due to premium savings.

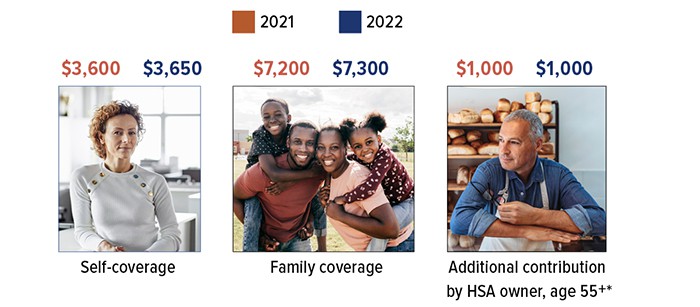

HSA Contribution Limits

Annual contributions to a health savings account may be made up to the April tax filing deadline of the following year. Moreover, any employer contributions must be included when calculating the annual contribution limit.

Your Choices and Preferences

Both PPOs and HDHPs encourage the use of in-network health-care providers. Moreover, if the plans come from the same insurance company, the provider network may be identical. Therefore, before enrolling, you should confirm that your preferred doctors and facilities participate in the network.

Additionally, consider your comfort level with the HDHP cost structure. Although an HDHP can reduce total costs over the course of a year, the higher out-of-pocket expenses at the time of service may cause some individuals to delay or avoid necessary care. Consequently, understanding your own health-care usage and risk tolerance is essential.

Health Savings Accounts

High-deductible health plans are specifically designed to pair with a tax-advantaged health savings account (HSA), which can be used to pay for eligible medical expenses incurred after the account is established. Typically, HSA contributions are made through pre-tax payroll deductions. However, in many cases, you may also make tax-deductible contributions directly to the HSA provider.

Furthermore, HSA funds, including any investment earnings when applicable, can be withdrawn free of federal income tax and penalties if they are used for qualified health-care expenses. Keep in mind that some states do not fully conform to federal tax treatment of HSAs.

HSA assets remain with you even if you change employers or retire. As a result, unspent balances can be carried forward or rolled over to another HSA and used to pay future medical expenses, regardless of whether you remain enrolled in an HDHP. However, you must be enrolled in an HDHP in order to open and contribute to an HSA.

1–3) Kaiser Family Foundation, 2020

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.