Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Pivots to Fight Inflation

On December 15, 2021, the Federal Open Market Committee (FOMC) of the Federal Reserve System made a significant shift in monetary policy in response to rising inflation. The Committee accelerated the reduction of its bond-buying program in order to tighten the money supply and projected three increases in the benchmark federal funds rate in 2022, followed by three more increases in 2023. Both steps were more aggressive than previous FOMC actions or projections.

To better understand how these steps may influence the U.S. economy, investors, and consumers, it helps to closely examine the Federal Open Market Committee’s tools and overall strategy. Furthermore, this perspective clarifies why recent policy decisions matter in the current economic climate.

Jobs vs. Prices

As the nation’s central bank, the Federal Reserve operates under a dual mandate that promotes price stability and maximum sustainable employment. Consequently, the Fed must strike a careful balance. An economy without inflation often stagnates and produces weak job growth. In contrast, a fast-growing economy with abundant jobs frequently faces rising inflation.

To manage this balance, the FOMC sets monetary policy in alignment with the Fed’s mandate. Specifically, the Committee established a 2% annual inflation target based on the personal consumption expenditures (PCE) price index. Moreover, the PCE index reflects a broad range of consumer spending on goods and services and typically runs lower than the more widely cited consumer price index (CPI).

The Committee allows PCE inflation to run moderately above 2% for a period of time. Consequently, this approach helps offset earlier periods when inflation remained below the target and supports long-term economic stability.

Inflation Trends and Policy Response

From May 2012 through February 2021, PCE inflation consistently stayed below the Fed’s 2% target. However, inflation accelerated rapidly afterward and reached 5.7% for the 12 months ending in November 2021, marking the highest level since 1982. By comparison, CPI inflation reached 6.8% during the same period.

Initially, Fed officials and many economists viewed inflation as transitory and tied largely to supply-chain disruptions caused by reopening the economy. However, the persistence and magnitude of inflation prompted policymakers to take corrective action. As a result, the Fed adjusted its outlook and strategy.

Despite recent concerns, officials continue to expect inflation to ease as supply-chain pressures resolve. Accordingly, they project a PCE inflation rate of approximately 2.6% by the end of 2022.

Key Economic Tool

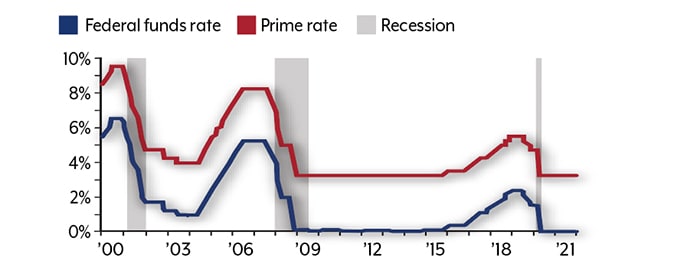

The federal funds rate serves as a primary tool for implementing monetary policy. It acts as a benchmark for many interest rates, including the prime rate that influences consumer borrowing costs. Therefore, when the Fed lowers the funds rate, it stimulates economic activity. Conversely, when inflation rises, the Fed increases the rate to slow demand and stabilize prices.

The Fed’s Toolbox

The FOMC relies on two main tools to balance employment and price stability. First, it sets the federal funds rate. Large banks use this overnight rate to lend to one another and meet Federal Reserve deposit requirements.

This rate also acts as a benchmark for other interest rates. For example, the prime rate that banks charge top customers usually sits about 3% above the federal funds rate (see chart). Consequently, it influences consumer borrowing costs such as credit cards and auto loans.

When the FOMC lowers the federal funds rate, it encourages economic growth and job creation. Conversely, when inflation rises, the Committee increases the rate to slow economic activity.

The Fed’s second tool involves Treasury bonds. It buys bonds to expand the money supply or lets bonds mature to reduce it. The FOMC purchases Treasuries through banks in the Federal Reserve System.

Instead of using existing deposits, the Fed credits banks’ balances directly. As a result, banks gain more funds to lend to consumers, businesses, and the government.

Shifting from Extreme Stimulus

When the economy shut down in March 2020 due to COVID-19, the FOMC took aggressive action. Its goal was to prevent a severe recession. The Committee cut the federal funds rate to a range of 0% to 0.25%.

At the same time, it launched a massive bond-buying program. Purchases peaked at $75 billion per day in Treasury bonds. By June 2020, buying slowed to $80 billion per month.

This pace continued until November 2021. At that point, the FOMC chose to reduce purchases gradually, with an initial end date of June 2022.5–6

In December, the Committee sped up the process. Consequently, the bond-buying program is now expected to end in March 2022. After that, the FOMC will likely consider raising interest rates.

Although the timing remains uncertain, projections suggest higher rates ahead. By the end of 2022, the rate may reach 0.75% to 1.00%. By the end of 2023, it could rise to 1.50% to 1.75%.7

Rising Interest Rates

The Fed now aims to slow inflation by moving toward a neutral policy stance. This shift signals confidence in the economy’s strength. If no further action is needed, the overall impact may remain modest.

The first rate increase likely will not occur until spring. Even so, higher rates raise borrowing costs for businesses and consumers. Consequently, corporate profits and household spending could decline.

Interest rates also affect bond prices. As rates rise, existing bond prices usually fall. This happens because new bonds offer higher yields.

However, higher rates can benefit certain investors. Bonds, CDs, and savings accounts may offer better returns. Retirees who depend on fixed income could see improved cash flow.

Traditional banks often adjust rates slowly. In contrast, online banks may respond more quickly by offering higher yields.8

As 2022 begins, inflation remains the primary concern. It is still unclear whether projected rate increases will curb rising prices. For now, investors may want to stay focused on long-term goals rather than react to short-term policy changes.

U.S. Treasury securities are guaranteed by the federal government for timely payment of principal and interest. Bond values fluctuate with market conditions. Bonds sold before maturity may be worth more or less than their purchase price. The FDIC insures CDs and bank savings accounts up to $250,000 per depositor, per institution. Forecasts depend on current conditions and may change.1, 4, 6–7) Federal Reserve, 2021

2) U.S. Bureau of Economic Analysis, 2021

3) U.S. Bureau of Labor Statistics, 2021

5) Federal Reserve Bank of New York, 2021

8) Forbes Advisor, December 14, 2021

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2022 Broadridge Financial Solutions, Inc.