Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Preparing for Libor to Leave the Building

The London Interbank Offered Rate (Libor) — once called the world’s most important number — is an interest-rate benchmark that has influenced borrowing costs for consumers, businesses, and investors around the world since 1986.1–2 From daily banker submissions, it has been quoted in five currencies (the British pound, the Swiss franc, the Euro, the Japanese yen, and the U.S. dollar).

Because LIBOR relies on bank quotes rather than actual transactions, banks could manipulate rates to their advantage. Consequently, a major scandal in 2012 revealed widespread manipulation. Moreover, LIBOR likely worsened the 2008 financial crisis.3

During the crisis, central banks sharply cut benchmark interest rates to reduce borrowing costs and support the global economy. However, LIBOR moved higher instead. As a result, borrowing costs increased when policymakers intended the opposite.

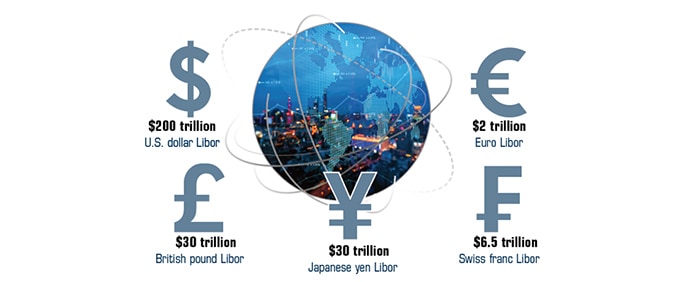

Replacing LIBOR is a complex task. Nevertheless, regulators continue working toward a more reliable benchmark to strengthen the global financial system. Currently, U.S. dollar LIBOR still determines interest rates on more than $200 trillion in financial products.4

These products include private student loans, credit cards, adjustable-rate mortgages, business loans, securities, and insurance contracts. Therefore, the transition away from LIBOR affects both consumers and institutions.

Deadline Looms

Some LIBOR settings stopped being published at the end of 2021. Others will remain available until June 2023. Consequently, many legacy contracts can mature before LIBOR is fully retired.

U.S. regulators instructed financial institutions to stop issuing new LIBOR-based contracts after December 31, 2021. However, institutions may continue referencing LIBOR for certain existing obligations until June 30, 2023.5

Role of the Alternative Reference Rates Committee

The Alternative Reference Rates Committee (ARRC) includes banks, insurance companies, and asset managers. The Federal Reserve Board and the Federal Reserve Bank of New York convened the group to guide the transition.

In 2014, ARRC began reviewing transition challenges and evaluating replacement rates. Subsequently, in 2017, it endorsed the Secured Overnight Financing Rate (SOFR) as the preferred benchmark.

Since then, ARRC has promoted an orderly transition. For example, it encourages SOFR adoption, recommends best practices, develops SOFR markets, and drafts fallback contract language. In addition, it proposes legislation to reduce legal uncertainty and publishes progress reports to track industry adoption.

Subject to Change

Face value of financial products benchmarked to Libor, by currency

New Benchmarks

Financial instruments that once relied on U.S. dollar LIBOR will now link to SOFR. Consequently, markets are shifting toward a more transparent and stable reference rate.

According to the ARRC, SOFR is a nearly risk-free rate based entirely on transaction data from the U.S. Treasury repurchase agreement market. Furthermore, regulators recommended SOFR because it supports most financial products and reflects significantly higher transaction volumes than other LIBOR alternatives.

6

At the same time, other central banks have introduced their own benchmarks. For example, the United Kingdom now uses the reformed Sterling Overnight Index Average, known as SONIA.

Credit-Sensitive Alternatives

Depending on the product, some financial institutions may reference credit-sensitive rates. These rates can better reflect lenders’ funding costs. However, regulators caution that alternatives other than SOFR could introduce risks similar to those seen with LIBOR.

7

Cost and Complexity of Transition

For institutions moving away from LIBOR, the transition process is complex and expensive. Specifically, firms must assess exposure, update risk models, revise contracts, and communicate changes to clients.

In addition, institutions must comply with new reporting requirements. As a result, analysts estimate that major banks will each incur transition costs exceeding $100 million in 2021 alone.

8

What Borrowers Should Know

Businesses and consumers with LIBOR-based adjustable-rate loans should closely review lender communications. Consequently, a switch to a new index may lead to a higher base rate and increased borrowing costs over time.

1, 4) Bloomberg, January 28, 2021

2–3) Forbes, August 10, 2021

5–6) Alternative Reference Rates Committee, 2021

7) The Wall Street Journal, August 16, 2021

8) Bloomberg, February 5, 2021

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2022 Broadridge Financial Solutions, Inc.