Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Social Security Spousal Benefits

More than 2.3 million Americans currently receive Social Security spousal benefits. The average benefit is almost $800 per month, and some spouses receive significantly more.1 These valuable benefits can make a big difference in funding retirement for a married couple and might result in higher total benefits, even if both spouses have their own work records.

Understanding Social Security Spousal Benefits

Spousal benefits can seem complex at first. Therefore, you should understand your eligibility and available options before filing. Furthermore, learning the rules helps you make informed financial decisions and maximize your retirement income.

These guidelines explain spousal benefits from the perspective of the individual applying for them. Consequently, you can better evaluate your retirement planning strategy.

Basic Spousal Benefit Eligibility Requirements

To qualify for spousal benefits, you must usually be at least 62 years old. Additionally, you must remain married for at least one year to a spouse who already receives or has filed for Social Security benefits.

The maximum spousal benefit equals 50% of your spouse’s primary insurance amount (PIA). This amount represents the benefit your spouse qualifies for at full retirement age. However, if you claim benefits before reaching full retirement age, your monthly benefit decreases permanently.

Furthermore, special eligibility rules apply to divorced spouses and individuals caring for dependent children. Therefore, reviewing your personal situation carefully helps ensure accurate benefit planning.

If your spouse claims benefits early, their worker benefit decreases permanently. However, your spousal benefit still uses their full primary insurance amount as the calculation base. Consequently, your benefit amount does not change due to their early filing decision.

Full Retirement Age and Its Impact on Spousal Benefits

Full retirement age (FRA) plays a critical role in determining both worker and spousal benefits. Therefore, understanding your FRA helps you choose the best time to file.

Full retirement age varies based on your birth year. For example, individuals born between 1943 and 1954 reach FRA at age 66. Meanwhile, those born between 1955 and 1959 reach FRA between 66 and 2 months and 66 and 10 months. Furthermore, individuals born in 1960 or later reach FRA at age 67.

Waiting until full retirement age allows you to receive the maximum spousal benefit. However, claiming earlier reduces your benefit permanently. Consequently, delaying your claim may increase your long-term financial security.

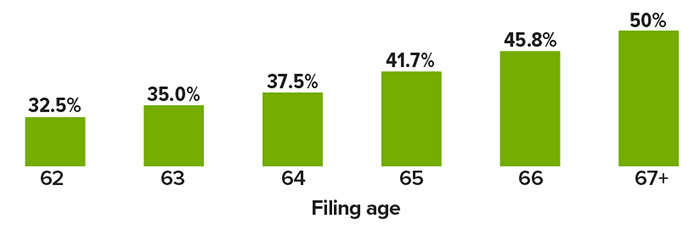

Spousal Benefit Percentage Based on Filing Age

Your spousal benefit percentage depends on when you file relative to your full retirement age. Therefore, filing at full retirement age provides up to 50% of your spouse’s primary insurance amount. However, filing earlier results in a reduced monthly benefit.

Careful timing can significantly improve your retirement income. Furthermore, planning ahead ensures better financial stability throughout retirement.

Percentages are adjusted incrementally for other FRAs or filing ages. If your birthday is the first day of the month, the Social Security Administration calculates your benefit as if you were born in the previous month.

Source: Social Security Administration, 2021

Spousal and Worker Benefits Coordination

If you qualify for both a spousal benefit and your own worker benefit, the Social Security Administration pays the higher amount. Therefore, you always receive the maximum benefit available based on your eligibility.

If you initially qualify only for your worker benefit, you may later qualify for a higher spousal benefit after your spouse files. Consequently, you receive an additional amount equal to the difference between your spousal benefit and your primary insurance amount (PIA). This increase is commonly known as the spousal boost.

However, if you claim your worker benefit before reaching full retirement age, your total combined benefit may remain lower. Therefore, timing plays a critical role in maximizing your Social Security income. Furthermore, individuals born after January 1, 1954, cannot switch later from a spousal benefit to a higher worker benefit.

Restricted Application Strategy

If you were born on or before January 1, 1954, you may qualify to file a restricted application for spousal benefits. This strategy allows you to receive spousal benefits while delaying your own worker benefit.

As a result, your worker benefit earns delayed retirement credits. These credits increase your benefit by approximately 8% per year until age 70. Therefore, delaying your claim can significantly increase your lifetime income.

Additionally, you can switch to your worker benefit at any time after filing the restricted application. Consequently, this approach may increase the total benefits received by both you and your spouse. Furthermore, you remain eligible even if your spouse filed early or was born after January 1, 1954, as long as you meet all requirements.

Benefits for Divorced Spouses

If you were married for at least 10 years and remain unmarried, you may qualify for benefits based on your former spouse’s work record. Importantly, your claim does not reduce or affect your former spouse’s benefits.

Eligibility begins when your former spouse files for benefits. However, if you have been divorced for at least two years, you may qualify even if your former spouse has not filed. Therefore, you do not need to wait indefinitely to receive benefits.

Additionally, you may continue receiving spousal benefits even if your former spouse suspends their benefits. However, this rule applies only to divorced spouses, not married spouses.

The maximum benefit equals 50% of your former spouse’s primary insurance amount. However, filing before full retirement age permanently reduces your benefit. Therefore, careful planning helps maximize your retirement income.

Spousal Benefits While Caring for a Dependent Child

If you care for a child under age 16 who receives benefits based on your spouse’s work record, you may qualify for spousal benefits regardless of your age. Therefore, this provision supports families with young dependents.

However, these benefits usually end when the child turns 16. Afterward, you may qualify again once you reach age 62 or meet other eligibility requirements. Consequently, understanding these timelines helps you plan effectively.

Factors That May Reduce Spousal Benefits

Your spousal benefits may decrease if you continue working before reaching full retirement age and exceed annual income limits. Therefore, monitoring your earnings helps avoid unexpected benefit reductions.

Additionally, benefits may decrease if you receive a pension from employment not covered by Social Security, such as certain government positions. Consequently, reviewing your complete retirement income sources helps ensure accurate benefit estimates.

Learn More About Spousal Benefits

For additional details, visit ssa.gov/benefits/retirement/planner/applying7.html. Furthermore, reviewing official resources helps you make informed retirement decisions.

1) Social Security Administration, 2021

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.