Denis Doulgeropoulos

Your Financial Professional & Insurance Agent

Your Social Security Statement: What’s in It for You?

The Social Security Administration (SSA) provides personalized Social Security Statements to help Americans age 18 and older better understand the benefits they will receive from Social Security. The Statement includes details about your earnings and estimates of your retirement, disability, and survivor benefits – information that can help you plan your financial future.

The Trustees of the Social Security Trust Funds publish annual reports to Congress to monitor the program’s financial condition and long-term outlook. According to the latest projections, the retirement program will have enough funds to pay full benefits only until 2033, unless Congress takes corrective action. Furthermore, the economic effects of the COVID-19 pandemic accelerated this projected shortfall by one year compared to earlier estimates. Therefore, policymakers and beneficiaries must pay close attention to future developments.

Report Highlights

Structure of Social Security Programs

Social Security consists of two primary programs, and each program operates through its own dedicated trust fund. Specifically, the Old-Age and Survivors Insurance (OASI) program provides monthly benefits to retired workers, eligible family members, and survivors. Meanwhile, the Disability Insurance (DI) program supports disabled workers and their families with monthly income. Together, these two programs form the combined system known as OASDI. Consequently, both programs play a critical role in providing financial stability for millions of Americans.

Combined Trust Fund Outlook

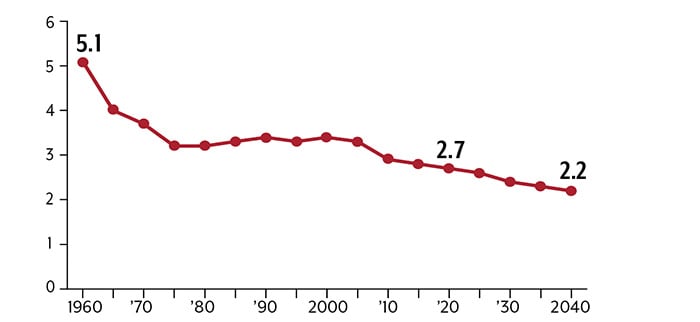

The Trustees reported that the total cost of the OASDI program exceeded its total income, including interest, beginning in 2021. As a result, the Treasury started using trust fund reserves to cover the funding gap. In addition, projections show that the combined trust fund reserves may run out by 2034. After that point, payroll tax revenue alone would cover only about 78% of scheduled benefits. However, the OASI and DI trust funds operate independently, so one program cannot routinely support the other. Therefore, both programs must maintain their own financial balance.

OASI Trust Fund Projections

The OASI Trust Fund, when evaluated separately, faces earlier depletion and may run out of reserves by 2033. At that time, payroll tax revenue would cover approximately 76% of scheduled retirement and survivor benefits. Consequently, future retirees could receive reduced benefits if lawmakers do not implement reforms. Therefore, long-term planning remains essential for individuals who depend on Social Security income.

Disability Insurance Trust Fund Outlook

The Disability Insurance Trust Fund also faces financial pressure and may deplete its reserves by 2057. This updated estimate reflects a depletion date that arrives eight years sooner than previous projections. Nevertheless, payroll tax revenue would still cover about 91% of scheduled disability benefits after depletion. As a result, the program would continue operating, although beneficiaries could receive reduced payments. Therefore, the DI program would still provide meaningful financial support.

Future Uncertainty and Legislative Impact

All projections rely on current economic assumptions and demographic trends. However, future economic changes, policy decisions, or legislative reforms could significantly alter these outcomes. Therefore, Congress may need to implement adjustments to preserve full benefits. Furthermore, individuals should remain informed and consider these projections when planning their retirement strategies.

Proposed Fixes

Lawmakers must address Social Security’s financial challenges as soon as possible. Early action allows gradual changes and reduces the burden on the public. Furthermore, combining multiple solutions could spread the impact more evenly. Therefore, policymakers may consider several strategic adjustments to strengthen the program’s long-term stability.

Increase Payroll Tax Rates

One option involves raising the current Social Security payroll tax rate, which stands at 12.4%. Currently, employees pay half, while employers cover the other half. Meanwhile, self-employed individuals pay the full amount. Experts estimate that increasing the rate by 3.36 percentage points would eliminate the long-term shortfall. Consequently, the total rate would rise to 15.76%. Alternatively, if lawmakers delay action until 2034, the required increase would reach 16.60%.

Adjust or Remove the Wage Ceiling

Another potential solution involves raising or eliminating the wage ceiling subject to payroll taxes. In 2021, this ceiling stood at $142,800. However, income above this level does not face Social Security taxes. Therefore, increasing or removing this cap would allow higher earners to contribute more. As a result, the program could generate additional revenue and improve financial sustainability.

Increase the Retirement Age

Policymakers could also increase the full retirement age beyond the current threshold of 67. Since people live longer today, extending the retirement age reflects modern life expectancy trends. Consequently, this adjustment would reduce total benefit payments and improve the system’s balance over time.

Reduce Future Benefits

Another option involves reducing future Social Security benefits. Experts estimate that lawmakers would need to cut scheduled benefits by about 21% to close the funding gap. Alternatively, they could reduce benefits by about 25% for individuals who become eligible later. Although this approach would strengthen program finances, it could significantly affect retirees’ income security.

Modify the Benefit Formula

Lawmakers could also revise the formula used to calculate benefits. For example, they might adjust how lifetime earnings translate into monthly payments. Consequently, this change could reduce overall benefit obligations while maintaining support for lower-income retirees.

Adjust Cost-of-Living Calculations

Another potential reform involves modifying the cost-of-living adjustment (COLA) formula. Currently, COLA helps benefits keep pace with inflation. However, policymakers could use a different inflation measure to slow benefit growth. As a result, the program could reduce long-term expenses while still protecting retirees from rising costs.

Pandemic Impact

The COVID-19 pandemic significantly disrupted Social Security’s short-term finances. During 2020, employment, earnings, interest rates, and economic output declined sharply. Consequently, payroll tax revenue dropped and placed additional pressure on the trust funds. However, economic activity began recovering, and payroll tax revenue rebounded faster than expected. Therefore, the overall damage remained less severe than originally feared.

In addition, demographic changes affected program projections. For example, mortality rates increased temporarily, while birth rates and immigration slowed. These shifts influenced long-term funding estimates. Nevertheless, economic recovery continues to strengthen Social Security’s financial outlook.

Furthermore, inflation surged during mid-2021, which increased benefit adjustments. As a result, beneficiaries expected one of the largest cost-of-living increases in decades. The Social Security Administration’s chief actuary projected a COLA increase of approximately 6.0% for 2022. Consequently, retirees received higher monthly payments to help offset rising living costs.

What Are the Stakes for You?

Early Retirement Trends

The COVID-19 pandemic pushed many older Americans into early retirement. The Census Bureau estimated that 2.8 million individuals aged 55 and older claimed Social Security benefits sooner than planned. In many cases, job losses or health concerns forced these decisions. Consequently, early claims often resulted in permanently reduced monthly benefits.

Options to Adjust Your Benefits

If you regret claiming benefits early, you may withdraw your application within 12 months. However, you must repay all benefits received before reapplying. Alternatively, if you reach full retirement age, you may suspend benefits voluntarily. As a result, your future monthly payments could increase. Therefore, careful timing can significantly improve your retirement income.

Importance of Social Security Income

Social Security benefits often represent a major portion of retirement income. Therefore, understanding your expected benefits remains essential. You can review your estimated monthly payments through your Social Security Statement. Furthermore, creating an online account allows easy access to your benefit information and projections.

Planning for Your Financial Future

Your retirement security depends on proactive planning and informed decisions. Although Social Security provides valuable support, personal savings remain essential. Therefore, you should build additional retirement income through investments and savings. Consequently, early preparation strengthens financial independence and long-term stability.

All information is from the 2021 Social Security Trustees Report, except for:

1) AARP, September 15, 2021

2) U.S. Census Bureau, 2021

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2021 Broadridge Financial Solutions, Inc.